It sounds almost harmless: a customer makes a purchase, changes their mind, and disputes the charge with their bank. But “friendly fraud”, also known as chargeback fraud or first-party misuse, is anything but friendly. And new research by PAYSTRAX reveals just how widespread, costly and underreported the problem has become for UK merchants, and how consumers view it.

PAYSTRAX latest whitepaper about friendly fraud, based on research among 1,000 UK consumers across all regions and age groups, shows that friendly fraud is not a marginal issue. It is a growing payments problem with real commercial consequences for merchants, retailers and subscription businesses. What we found should concern every business that accepts card payments.

What is friendly fraud?

Friendly fraud occurs when a customer makes a legitimate purchase and then disputes the transaction with their bank or card company, claiming the charge was fraudulent, that they never received the goods, or that they didn’t authorise the payment. The bank issues a chargeback, the merchant loses the sale and pays a chargeback fee, and the customer keeps the money.

It also goes by other names: chargeback fraud, first-party fraud, or first-party misuse. Whatever you call it, the impact on merchants is the same.

Some cases are genuinely accidental: a customer forgets they made a purchase, doesn’t recognise the merchant name on their statement, or fails to cancel a subscription before being charged. But a significant and growing proportion is deliberate. And in both cases, merchants bear the full financial cost.

The scale of the problem: what our research found

PAYSTRAX commissioned independent third-party research into consumer attitudes and purchasing behaviours across all UK regions and age groups. The results were striking.

22.3% of UK consumers have knowingly asked their bank to refund a legitimate transaction in the past year. More than one in five Brits have purposefully initiated a chargeback for something they genuinely bought and, in many cases, kept. A further 22% did so unknowingly – forgetting a purchase or failing to unsubscribe from a free trial.

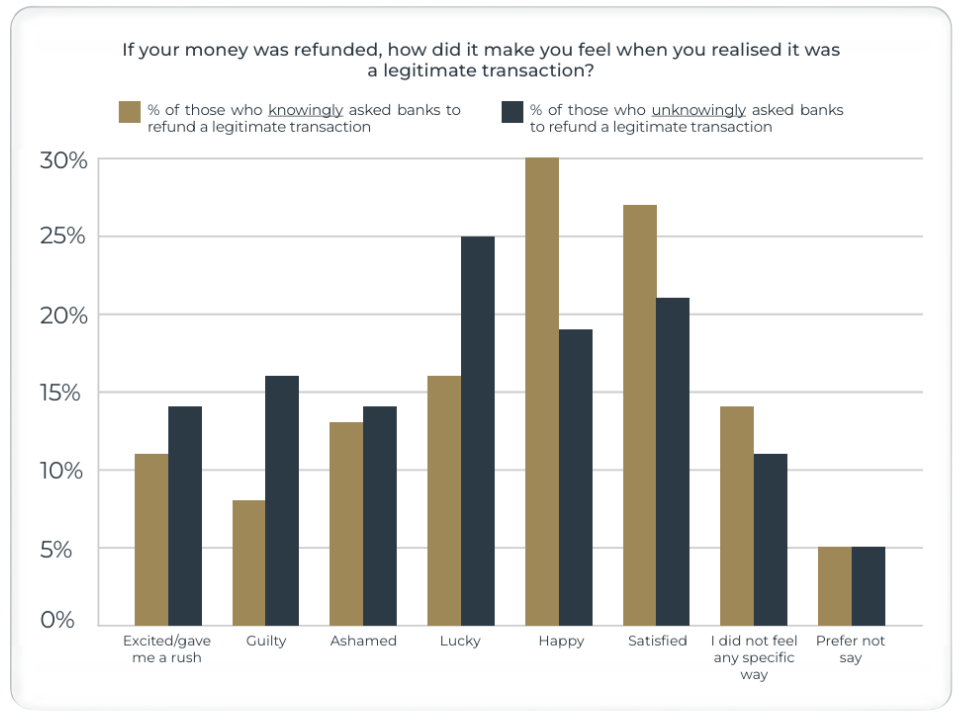

But here’s where it gets worse. Of those who accidentally triggered a chargeback, over a third (35.71%) still kept the money after realising the transaction was legitimate.

On the emotional side, the data is equally troubling. Of consumers who knowingly committed friendly fraud, more than six in ten (62.84%) felt pleased about the outcome. Just 13.51% admitted feeling guilty or ashamed. For those who did so accidentally, more than half (57.14%) still felt positively about the refund.

These aren’t edge cases. This is the norm.

Who’s actually responsible and who pays?

We also asked consumers who they think is responsible for verifying whether a disputed transaction is genuinely fraudulent. The answers reveal a fundamental accountability gap at the heart of the payments system.

📊 28.6% said no one in particular is responsible

📊 26.1% said it’s up to the banks to prove it

📊 19.2% said the customer should own up to it

📊 15.1% said it falls to Payment Service Providers or card acquirers

📊 10.1% said it’s up to the retailers

While consumers point the finger at banks, in practice it is merchants who absorb the cost. Banks issue the chargeback form, pass liability down to the merchant, and lose nothing themselves.

Jóhannes Ingi Kolbeinsson, Group CEO and co-founder of PAYSTRAX adds:

While Britons view banks as the single most responsible entity, in reality, banks tend to push the liability down the line. If a customer requests a chargeback or complains about a transaction, the bank tends to give them a form to claim the money back from the merchant. The bank itself doesn’t lose anything.

What’s driving friendly fraud?

Several structural factors make friendly fraud not just possible, but easy.

The chargeback process has almost no barriers for cardholders. In the current system, a consumer doesn’t need to provide any evidence – such as a police report – to claim that a transaction was fraudulent. The merchant, meanwhile, gets little to no opportunity to dispute the claim, even with proof of a legitimate transaction.

Card schemes push the ‘fraud’ button. Payment network policies encourage card issuers and cardholders to label even accidental disputes as “fraudulent.” This misrepresents what fraud actually means and, in effect, normalises dishonesty in the refund process.

Subscriptions are a major contributor. Subscribers may forget they signed up, find cancellation too complex, or simply file a fraud claim as a shortcut out of an unwanted service. The result is the same: the merchant loses revenue and gets flagged.

Visa’s VAMP programme adds further pressure. Visa’s new fraud-prevention rules penalise merchants who exceed a set dispute ratio – with fines, increased monitoring, or restrictions on their ability to process payments. This means even a modest level of friendly fraud can have serious operational consequences for businesses that did nothing wrong.

Globally, friendly fraud now accounts for up to 75% of all chargebacks, according to Visa. Merchants worldwide lost more than $117 billion to chargebacks in 2023 alone. In the UK, Chargebacks911 estimates the annual cost to merchants exceeds £128 million.

Jóhannes Ingi Kolbeinsson is direct about where responsibility lies:

In my view, we should define intentional chargeback claims for legitimate purchases as outright stealing. <…> Card companies equate first-party misuse (friendly fraud) to criminal fraud, yet they’re driving cardholders to click the ‘fraud’ button in order to get a refund. In that case, are global payment networks – and I’m being a little sarcastic here – intentionally promoting organised crime?

Four trends reshaping the friendly fraud landscape

Our research points to four key dynamics that merchants, payment providers and regulators need to understand.

1️⃣ Chargeback requests need clearer accountability

Most people aren’t sure who’s responsible for verifying whether a dispute is genuine. That confusion enables friendly fraud to thrive. A coordinated education campaign and standardised communication framework between banks, PSPs, and merchants would go a long way in reducing both the cases and the confusion.

2️⃣ Merchants carry the hidden cost

Consumers largely blame banks for fraudulent transactions. But it is merchants who routinely absorb the full cost. Only 10% of our survey respondents think retailers are responsible for proving fraud – yet the card payment ecosystem consistently lands the liability there. These distorted consumer protection policies are eroding merchant margins and incentivising misuse.

3️⃣ A “finders, keepers” mindset fuels false chargebacks

Consumers often don’t view an illegitimate refund as wrongdoing, they see it as beating the system. One in three (30.41%) feel happy when they purposefully commit friendly fraud. This is a consumer behaviour problem as much as an economic one. Greater transparency about the direct impact on merchants could help reframe “lucky” refunds as what they actually are: theft.

4️⃣ Digital natives are most likely to ask for refunds

40% of 16–24-year-olds have knowingly asked their bank to refund a legitimate transaction in the past twelve months as compared to just 5% of those aged 55 and over. Gen Z are twice as likely to commit friendly fraud as Gen X. The practice risks becoming a sport among younger consumers, with the hope of winning free products and services through banking apps. Stronger education and clearer processes are essential to reversing this trend.

What needs to change?

Friendly fraud will not fix itself. The real responsibility lies on the card scheme duopoly to change both the terminology and the enforcement of this type of fraud. At PAYSTRAX, we’ve outlined six steps we believe the industry must take:

- Reclassify friendly fraud transactions as “cardholder disputes” rather than fraud

- Enable merchants to respond, refund, or resolve issues directly with the cardholder before penalties are applied

- Require cardholders to present a police report or similar evidence when registering a fraudulent transaction

- Exclude friendly fraud transactions from merchants’ fraud ratios if they refund in good faith

- Stop equating these disputes with criminal fraud — this unfairly criminalises merchants while giving cardholders a free pass

- Create a simple subscription termination system within banking apps, similar to Apple’s subscriptions hub on iPhones

How PAYSTRAX supports merchants

At PAYSTRAX, we work directly with our merchants to help minimise exposure to chargebacks and friendly fraud. Our team reviews merchant ratios to spot patterns of high dispute activity, then works collaboratively to address root causes – whether that’s improving how charges appear on bank statements, clarifying unsubscribe processes, or updating website information to reduce ambiguity.

We believe the system doesn’t have to be this broken. Small changes in terminology and process can protect businesses from unfair reputational damage and financial penalties, while still preserving genuine consumer rights.

Full research about friendly fraud

Our complete whitepaper Not-so-friendly fraud: When customers become criminals – covers the full survey findings, consumer attitudes data and our detailed recommendations for the industry.

➡️ Download the full PAYSTRAX friendly fraud whitepaper here ⬅️